SHORT NOTES: 1/23/2026

Everyone's Winning, Retail Power, The Big Money Trade, and much more.

Good morning and happy Friday — hope everyone had a great week.

In today’s edition:

✅ My collection of this week’s BEST charts and articles “heard on the street”.

✅ *And adding a few of our own.

Let’s get started…

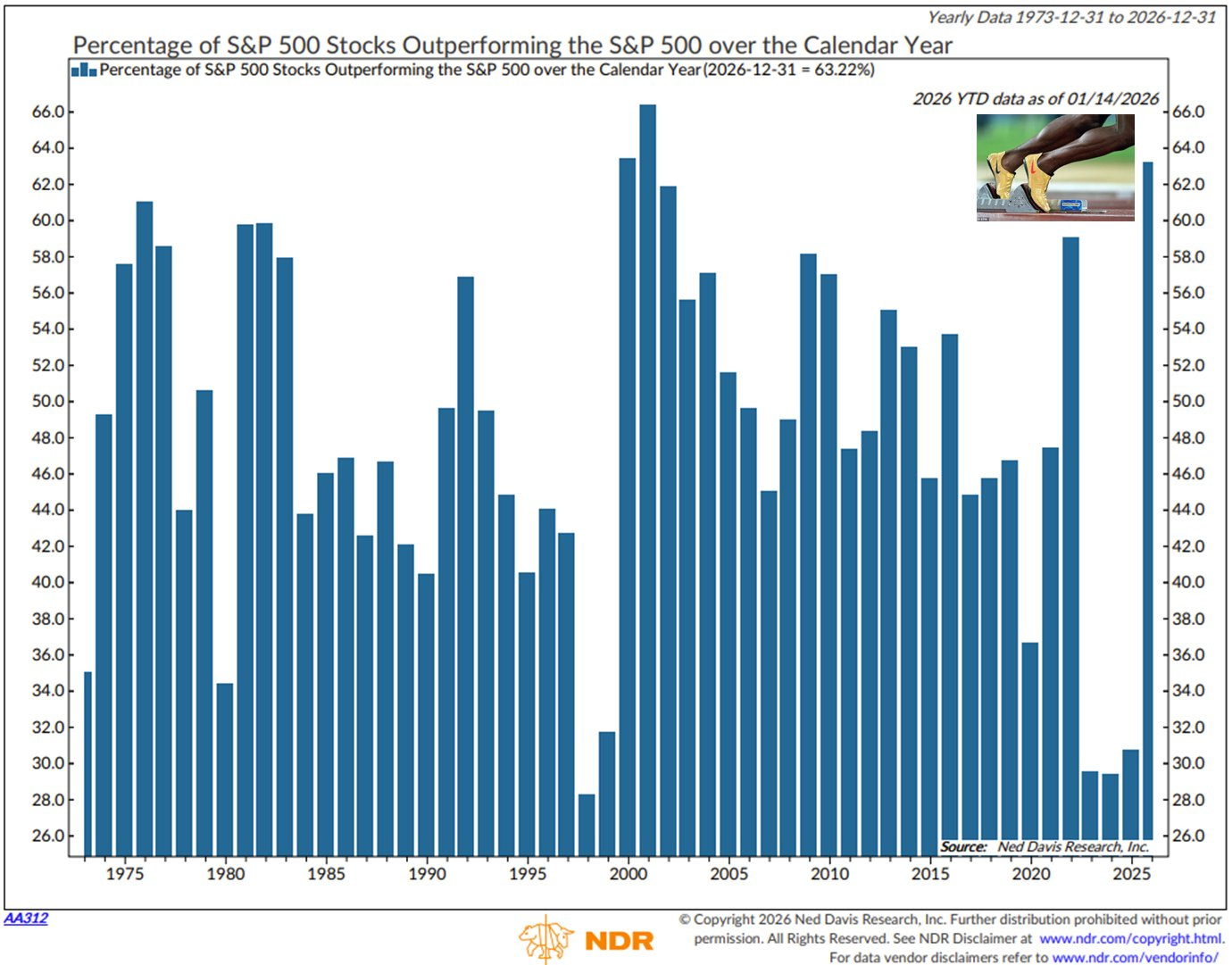

1. Everyone’s Winning.

63% of S&P 500 stocks are beating the index YTD (NDR, Jan 14).

This is the best market participation since 2001.

On Wednesday’s close, this number rose to 65% — the second best in 50 years.

*Will the market’s strength continue?

✅ Let’s talk about that record spike in 2001…

That was a Bear Market, with some fascinating stats:

S&P and NDX fell 13% and 33% that year. Meanwhile the Equal-weight S&P was down 2%, and the Russell was UP 1% — a big outperformance from the “Smalls”.

Critically, 37% of S&P stocks closed UP in 2001, 25% gained more than +10%, and 20% gained more than +20% that year. Amidst a Bear Market.

All told, 2001 was an excellent year for active management.

What does this mean for 2026…?

✅ This chart ties closely with our (1) 2026 framework, (2) diversification strategy, and (3) thematic allocations.

✅ “When everything is leading, pure diversification wins.”

✅ Remember: momentum was KING in 2025, and 2026 could be even stronger.

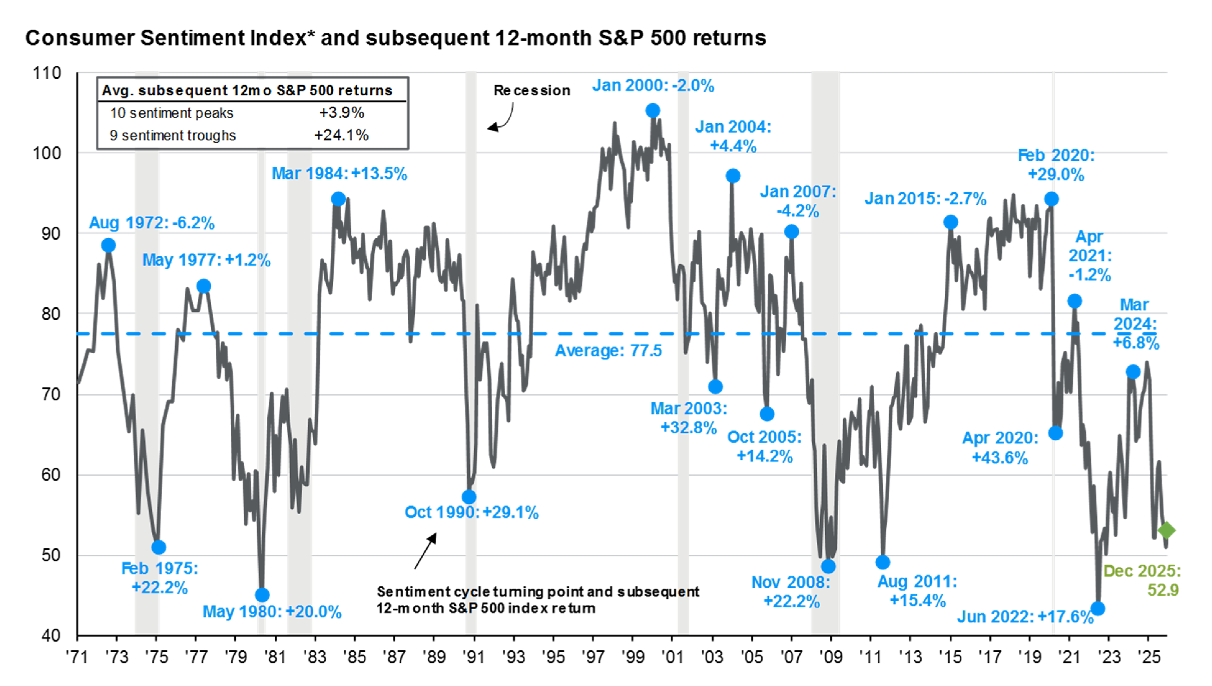

2. The Sentiment Economy.

Building on recent themes, and thinking about stocks vs. the economy:

Here’s another great chart to keep in mind…

✅ When consumer sentiment was near these levels, forward stock returns were outstanding.

✅ Meanwhile, leading stocks and groups in our Core Watchlist are making new highs.

How will this divergence be resolved?

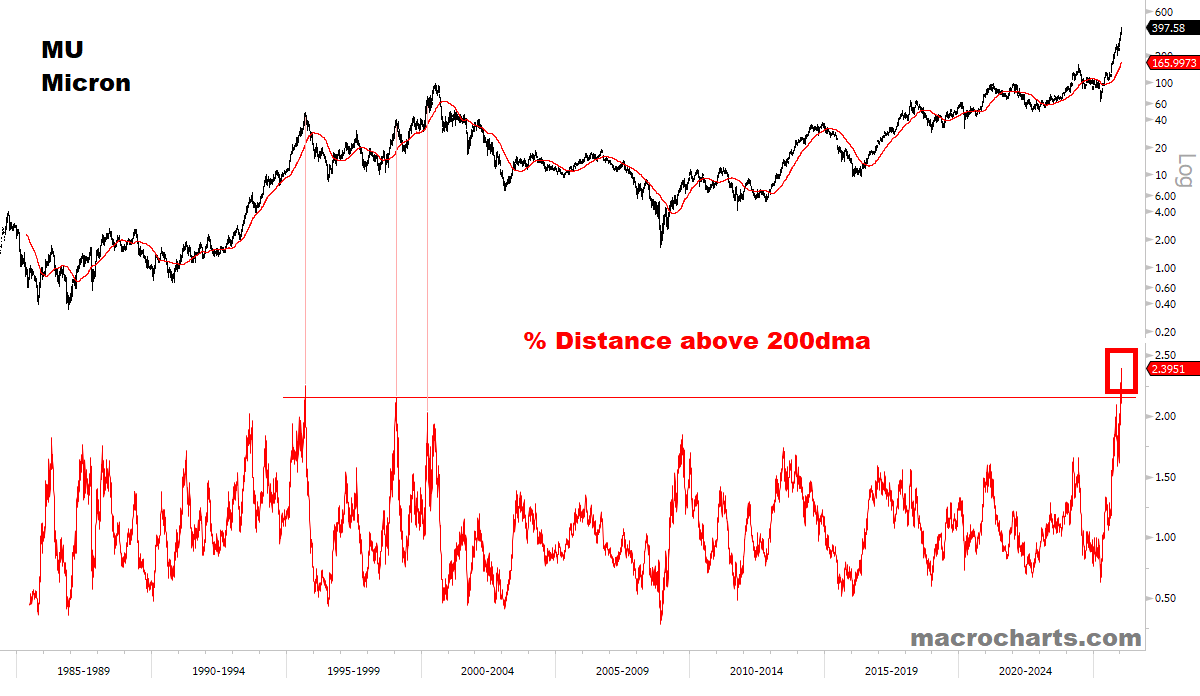

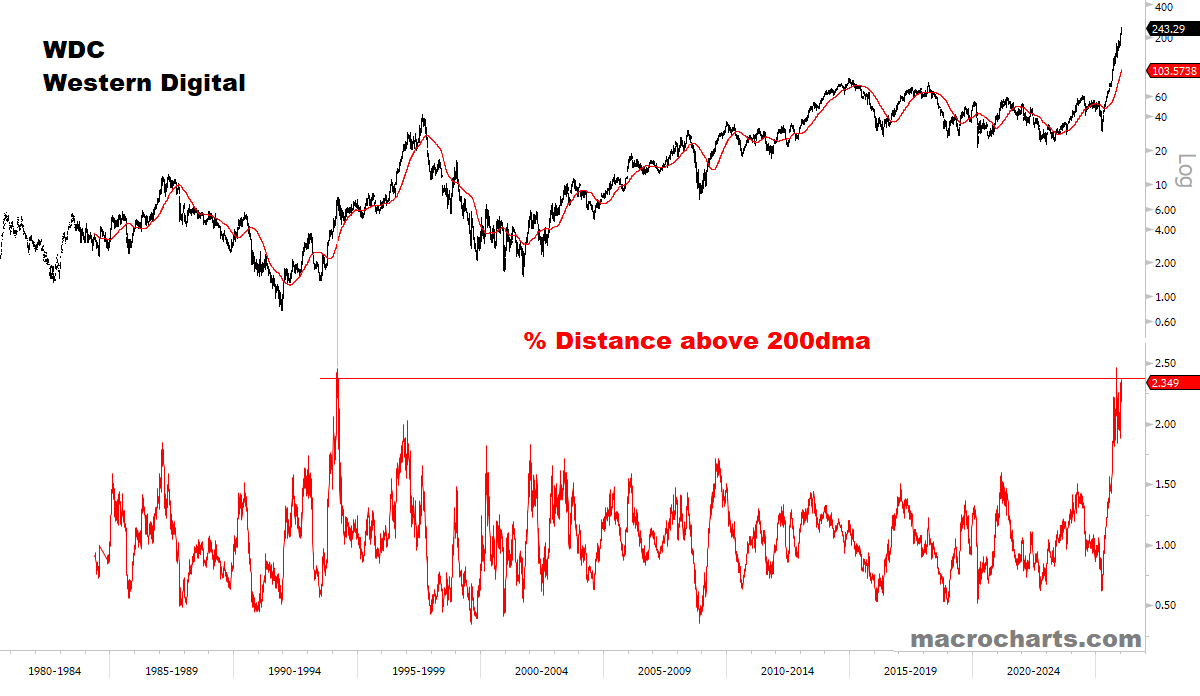

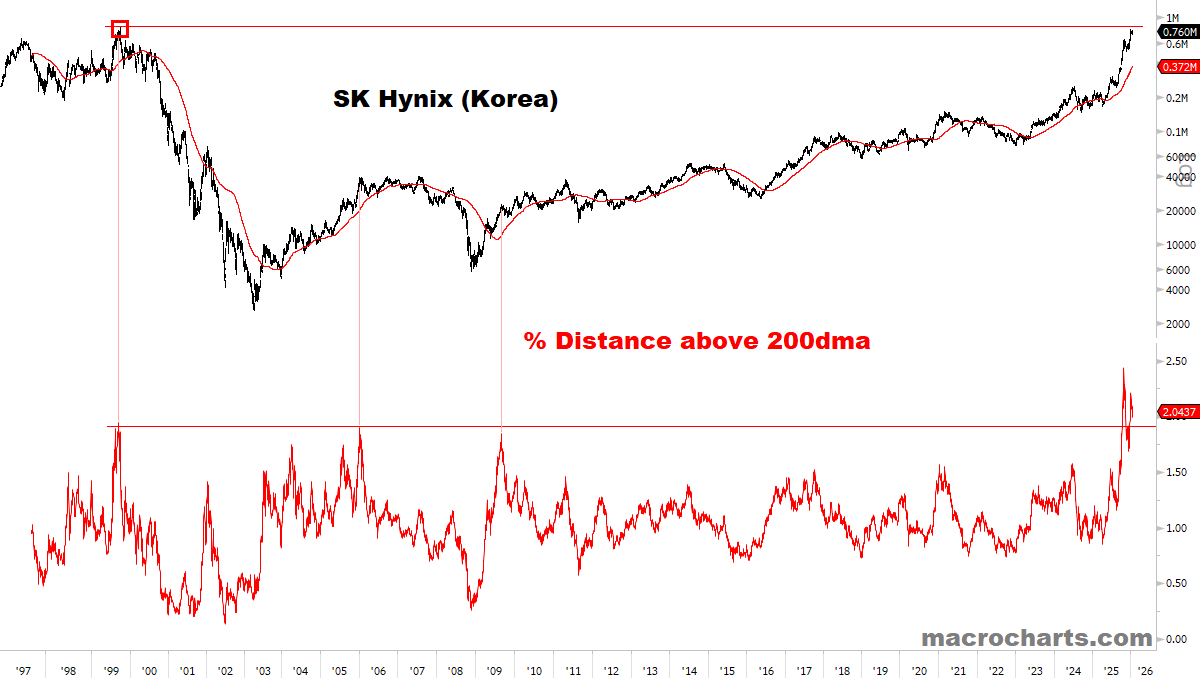

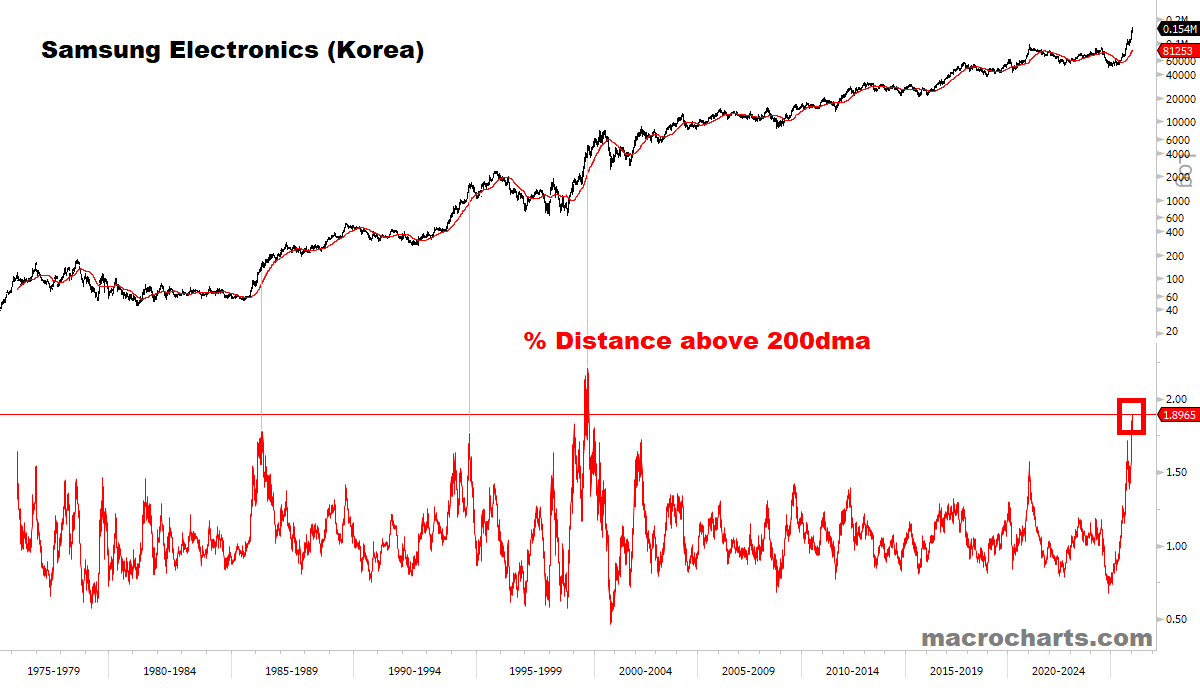

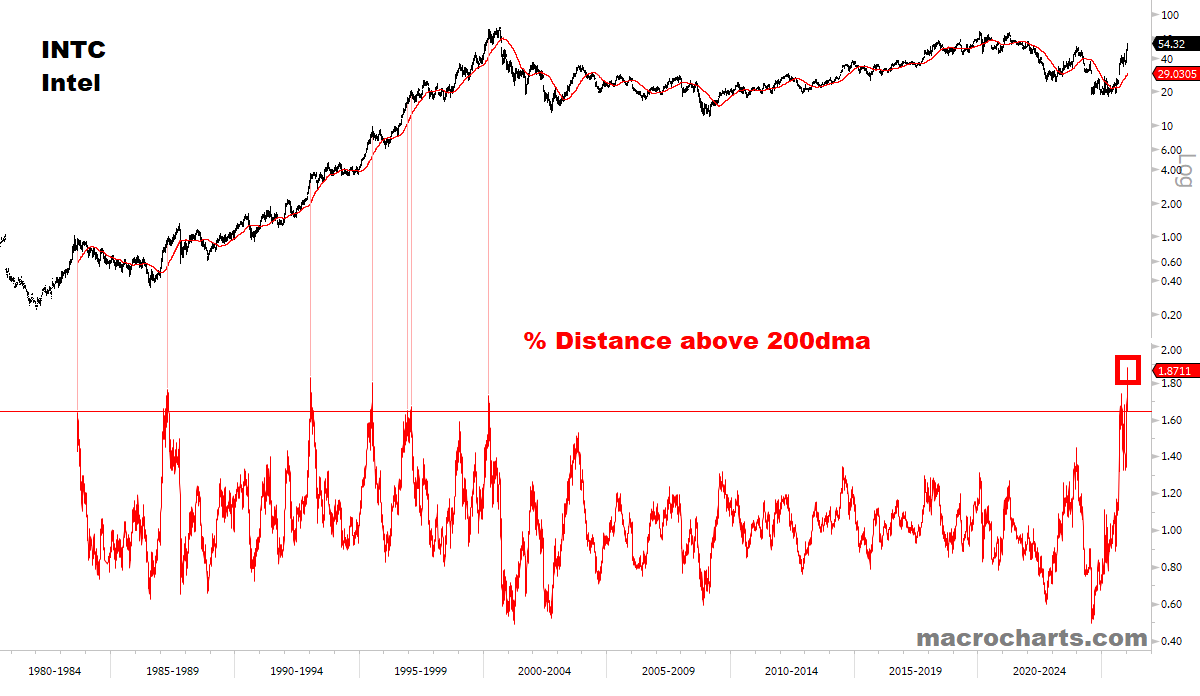

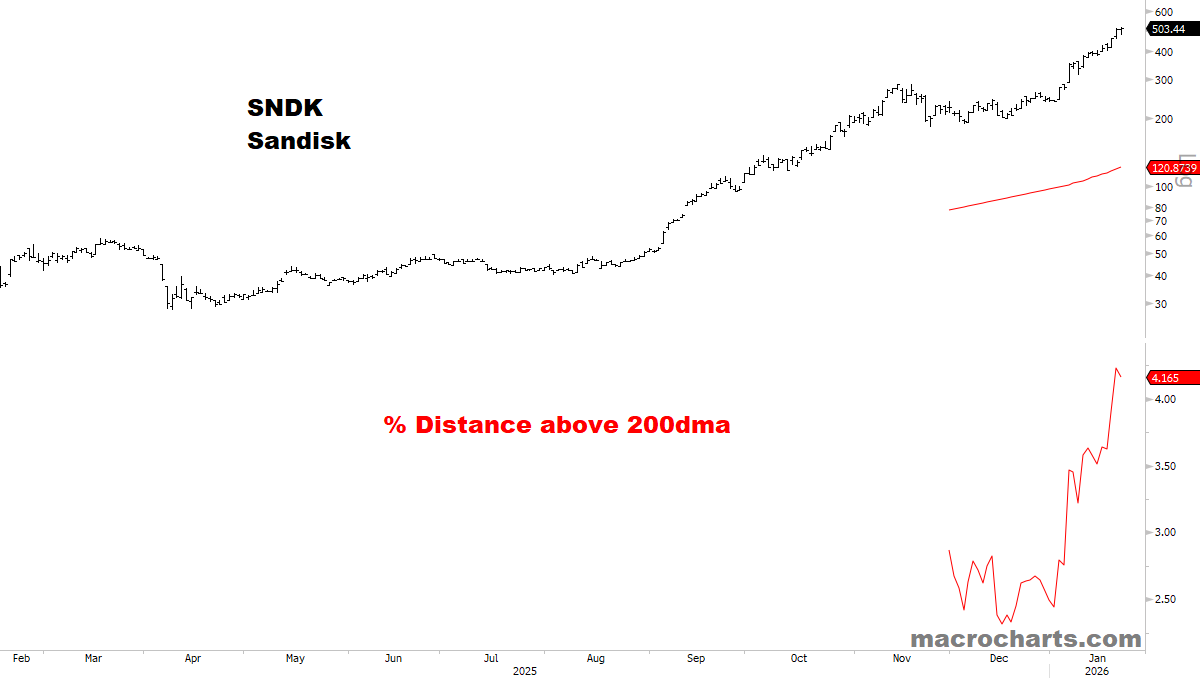

3. Memory on Fire.

Memory & Storage stocks are in pure acceleration mode:

Micron (one of our best performers last year), is now THE most stretched in its entire 40-year history (including the Internet Bubble):

This is the market saying:

There’s no precedent for what Micron’s business is going through today.

Or is there?

Let’s look at the rest of the global group — relative to their history:

Related:

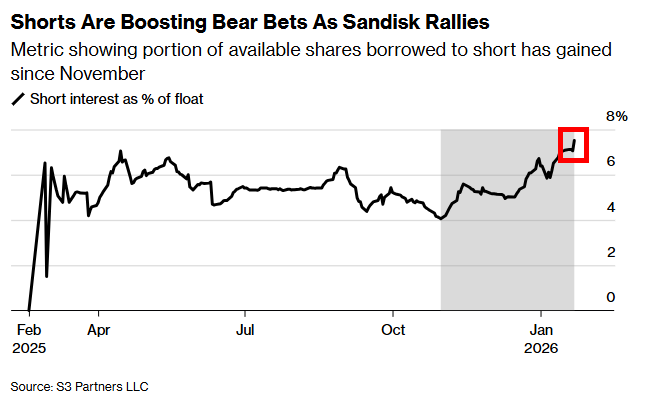

“Shorts Are Boosting Bear Bets As Sandisk Rallies” (Jan 23)

“Short interest in Sandisk has been climbing for months alongside a sharp rally in the stock, pushing the risk of a short squeeze to an ‘extreme’ level” (source: S3)

Short interest has risen to 7.5%, with losses on short positions reaching roughly $3 Billion

“Short sellers have moved in lockstep, shorting aggressively into the rally”

How far can these stocks run?

✅ I’ll say “keep your charts close, and your trailing stops closer.”

✅ We’ll comment more on this soon — and will be watching as these trends develop.

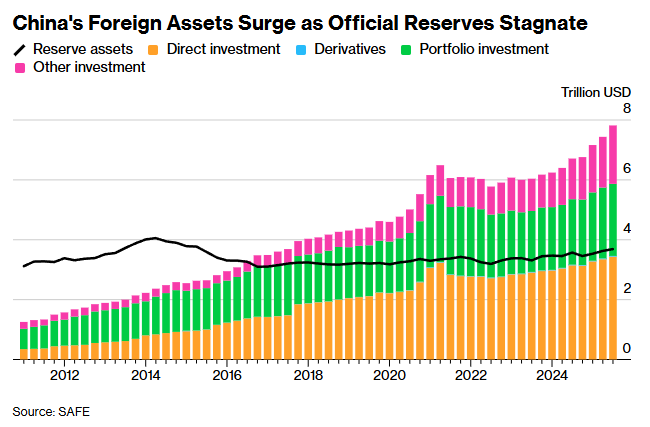

4. China — some top articles worth highlighting:

US and China Flip the Global Script as Capital Flows Reverse (Jan 11)

“As the US draws back, China is again dispersing capital globally, leading the rest of the world to confront a fundamental change in their economic relationships with both superpowers.”

“It’s a nascent trend that’s only just starting to show up in the data. In the first half of 2025, the value of outbound investment from China into the rest of the world overtook that coming from the US and accounted for 10% of the global total, according to OECD data. At the same time the US sucked up a fifth of all inbound investment around the world as the European Union saw a 45% decline compared with six months earlier.”

“Greenfield projects accounted for more than 85% of the $106.6 billion in outbound Chinese investment announced in the first three quarters of 2025”

“The changing patterns reflect widening global imbalances. China’s outbound investment is a consequence of a trade surplus that has continued to grow as efforts to increase domestic consumption falter and Chinese companies seek new markets. Where once China’s trade surplus ultimately ended up in US Treasuries via a state-controlled system, the capital is now funding new foreign factories.”

China’s $1.2 Trillion Windfall Quietly Seeps Into Global Markets (Jan 16)

A record trade surplus in China is leading to massive private purchases of overseas securities and business expansion abroad, with some two-thirds of foreign assets sourced from global trade ending up with companies, individuals, and state lenders.

Investors in China’s non-official sector saw their holdings of assets abroad soar by more than $1 trillion in the first three quarters of last year, with a $535 billion surge in Chinese private purchases of overseas securities like US stocks and European bonds.

The shift in China’s foreign assets from the central bank to the private sector is ushering in a new era of global capital flows, with risks of a sudden capital reversal and increased sensitivity to yuan appreciation, and potentially leading to a global financial system reliant on liquidity sourced from China.

China’s $7 Trillion Cash Pile Is Shifting Into Stocks, Gold (Jan 18)

*This article ties closely with our 2026 framework reports (link).

Chinese households are looking for higher-yielding investments as roughly $7 trillion in time deposits come due this year.

Investors are considering moving into stocks, wealth management products or insurance, which would support Beijing’s efforts to cultivate sustainable market gains.

The shift is already underway, with demand for participating insurance policies and stocks increasing as investors seek steady returns in a low interest rate environment.

Alibaba Is Said to Plan IPO for AI Chipmaking Unit T-Head (Jan 22)

Alibaba Group Holding Ltd. is preparing to list its chipmaking arm, tapping strong investor interest in the AI accelerator business.

Alibaba’s chip endeavor is part of its broader campaign to become a leading AI company, with the company having pledged more than $53 billion toward infrastructure and AI development.

BABA has posted a strong start to 2026, up +30% YTD (still our top China Tech holding) — looking for pullbacks to add tactical exposure, and will update along the way:

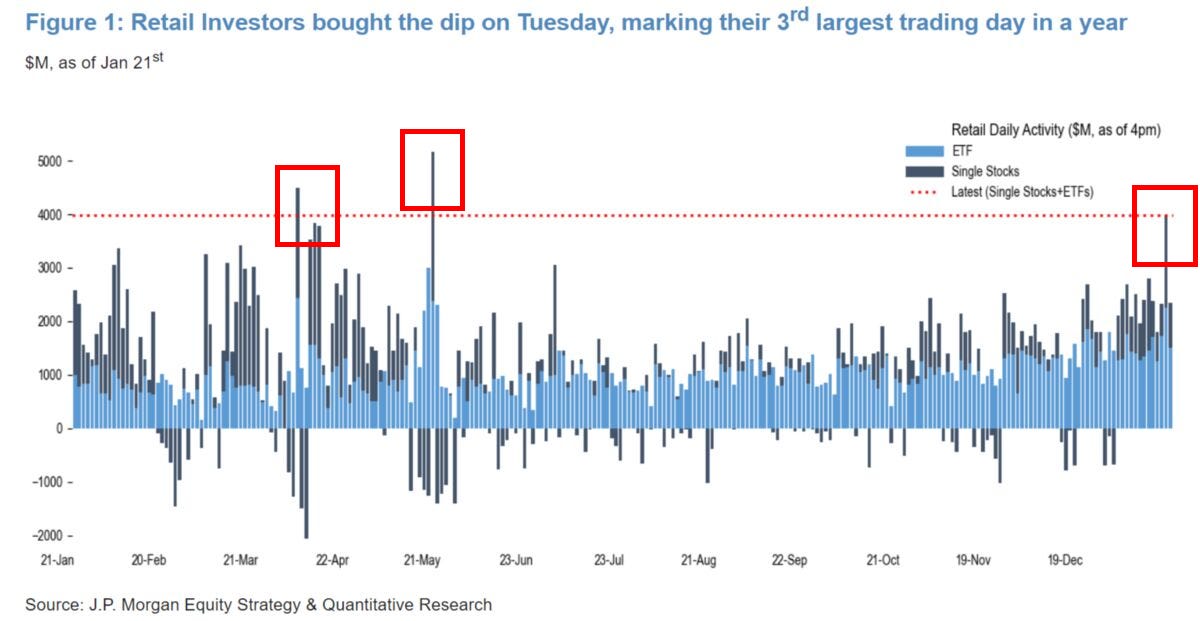

5. Retail Power.

Tuesday was the worst day for the major ETFs since April 2025:

Retail investors seized the opportunity:

“Retail Investors Spent Records on Buying the Dip” (JPM)

Tuesday saw the *third largest* buying spike from retail investors in a year.

“This is comparable to last year’s buy-the-dip episodes in April.”

✅ In our next reports of the series, we’ll compare the current environment to prior cycles in history — and the potential (big) implications for 2026.

Stay tuned.

Below, my favorite article this week (in case you missed it), some fascinating charts on investor preferences — and the “Big Money” contrarian opportunity (of this decade?)…

Keep reading with a 7-day free trial

Subscribe to Macro Charts to keep reading this post and get 7 days of free access to the full post archives.