SPECIAL REPORT: HURRICANE WATCH

BATTENING DOWN FOR 2025.

EXECUTIVE SUMMARY

Looking beyond key Tactical signals we’re tracking, I want to start thinking about next year…

What could 2025 look like?

This Special Report is a study of important core concepts:

Hurricane Years — historical patterns and their signals.

What 2025 could look like from a Market & Sector perspective, and more importantly — looking through history, what kind of Volatility is possible.

As some key Stock groups are warning, we could be entering an opportunistic *targeted* Short-selling environment — something which Investors have forgotten entirely / are unprepared for.

This comprehensive report will outline my Core playbook and Timing strategy for what may be ahead — including the signals and scenarios I’m watching, to manage a focused Long/Short portfolio next year.

Last, we’ll cover the data to watch, and what signals would increase conviction that a storm is coming.

Save this report for future reference — we’ll revisit these core ideas throughout 2025.

Let’s get started:

HURRICANE YEARS

What are Hurricane Years?

They’re an upheaval of consensus narratives and crowded positioning.

Sectors and Stocks move violently in all directions, with extreme force — some straight up / some straight down / others chopping with high Volatility.

There are EXTREME winners and losers — and they TREND for most (if not all) of the year (*Remember this key concept).

A few losing Groups can drop 30-70%. There is no floor for oversold. They should be avoided the entire year — the only optimal strategy is to Short bounces.

A few winning Groups can gain 30-70%. There is no ceiling for overbought. They should not be Shorted — the only optimal strategy is to Buy pullbacks.

If you’re a passive Index investor, or if you’re Long some winners / Short some losers, it’s like being in the EYE of the hurricane. But it requires patience and discipline.

Hurricane Years have LOW Total Return and HIGH Volatility (the opposite of 2024).

The FIRST HALF of Hurricane Years are generally OK — single-digit S&P returns with some initial Volatility, though nothing extreme.

Under the surface however, there’s massive turbulence across Sectors.

In the FIRST HALF, usually in the FIRST QUARTER, the year’s biggest losers are generally revealed. Sometimes they start fading in December (before the new year) — which is why I’m watching for weakness NOW. (*More on this shortly.)

The SECOND HALF of Hurricane Years are difficult — the accumulated Sector weakness is so great that the Indexes finally get the memo, and the winners get dragged down briefly too. Typically, this is when the biggest drawdown of the year occurs (a Correlation-1 decline).

Since 2009, Hurricane Years have occurred roughly every 3-4 years:

Stocks have a tough year sometimes — it happens.

Every few years, things get extended and frothy (like now) — then something comes along to disrupt things, creating Volatility.

This year delivered one of the highest Sharpe ratios ever — with High-Return and Low-Volatility.

Asset Managers are pushing the risk curve with aggressive positioning.

Stock Margin and Leverage are increasingly rapidly (recently, even the CEO of IBKR expressed concern over this).

Traders have record Long exposure in Futures & ETFs, while juicing Options speculation to historic levels (similar to late 2021).

Though not an exact repeat of 2021’s Bubble (no SPACs or people buying pictures of rocks) — we can recognize similar excesses today.

So what could next year look like?

Let’s say 2025 could be “tough”. A low, or even negative S&P return, with unusually high Volatility — the opposite of this year.

Historically, how did that look like?

Like this:

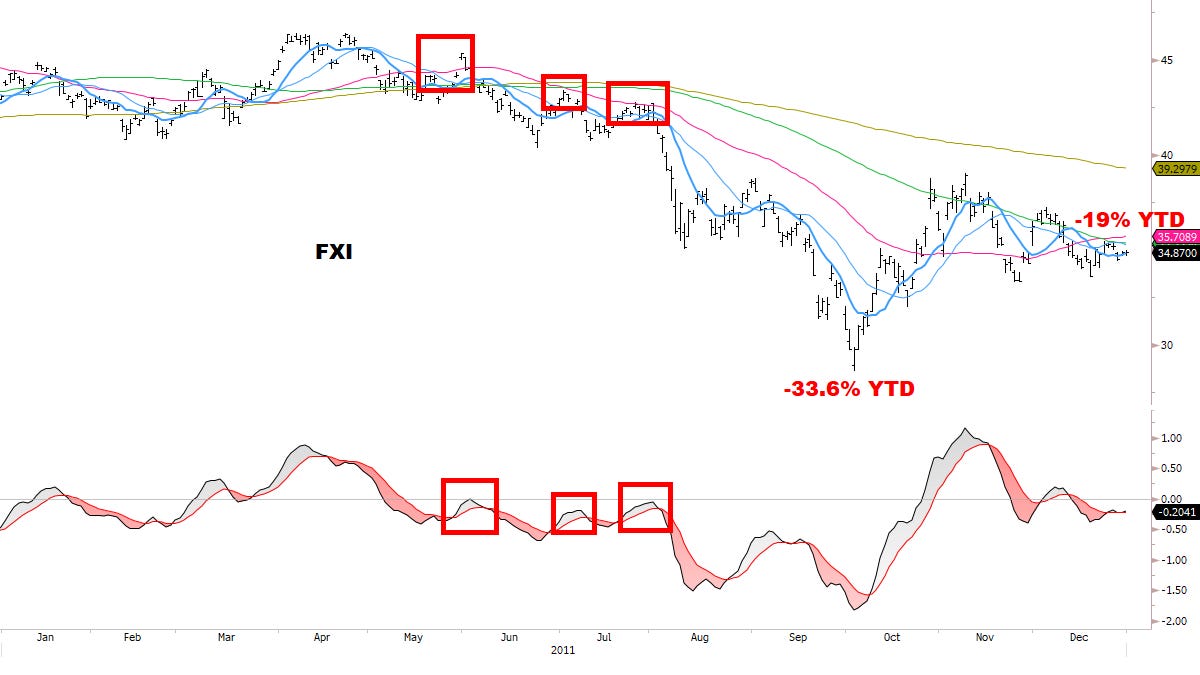

2011

Worst-performing (candidates for Short book):

Best-performing (candidates for Long book):

Additional 2011 returns for reference:

#2 Best-performing Sector: XLP +10.9% (Defensive sector)

#3 Best-performing Sector: XLV +10.1% (Defensive sector)

Almost everything else performed in-line or worse than the S&P.

VIX 2011 high: 48.

Remember this pattern:

The weakest Sectors typically failed early in the year,

were the first to break their uptrends,

staged several failed bounces,

and were ultimately the biggest % decliners of the year.

They gave multiple warnings all the way down, and closed near the lows of the year.

Their weakness didn’t matter for the Stock Market, *until it did*.

The winners were also revealed early — and remained consistent throughout the year.

In summary: a “WINNER TAKES ALL” year.

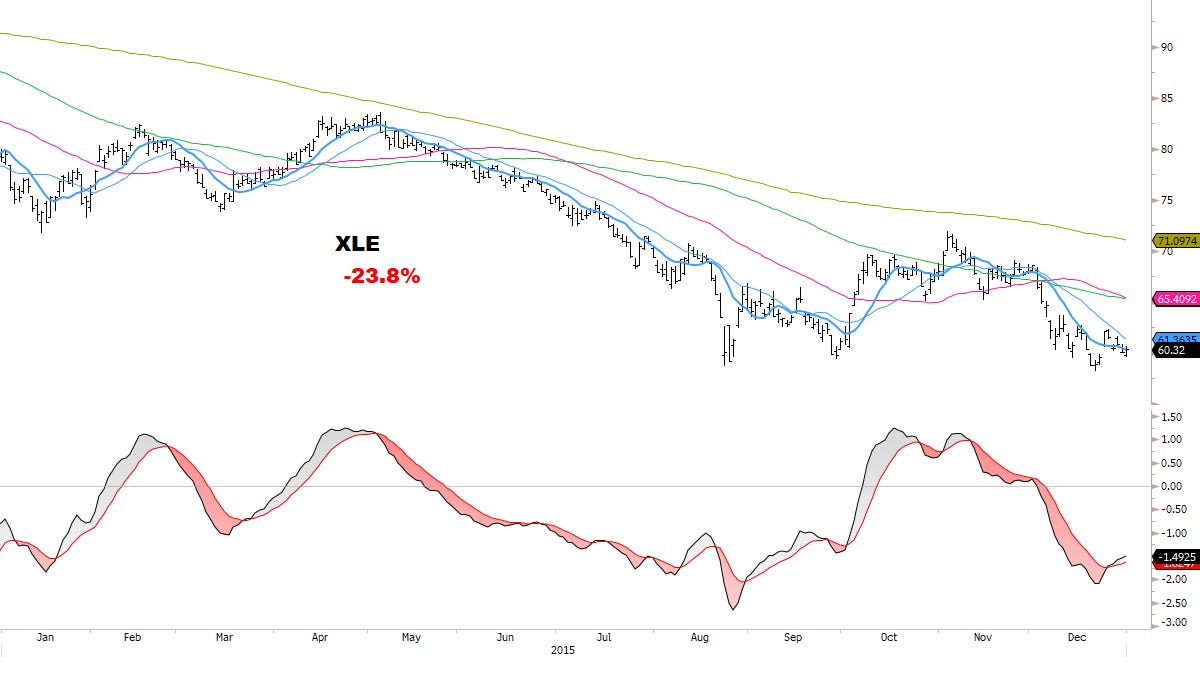

2015

Worst-performing (candidates for Short book):

Best-performing (candidates for Long book):

Additional 2015 returns for reference:

Biotech +12.0%

NDX +8.4%

Almost everything else performed in-line or worse than S&P.

VIX 2015 high: 53.

Another year of “WINNER TAKES ALL”.

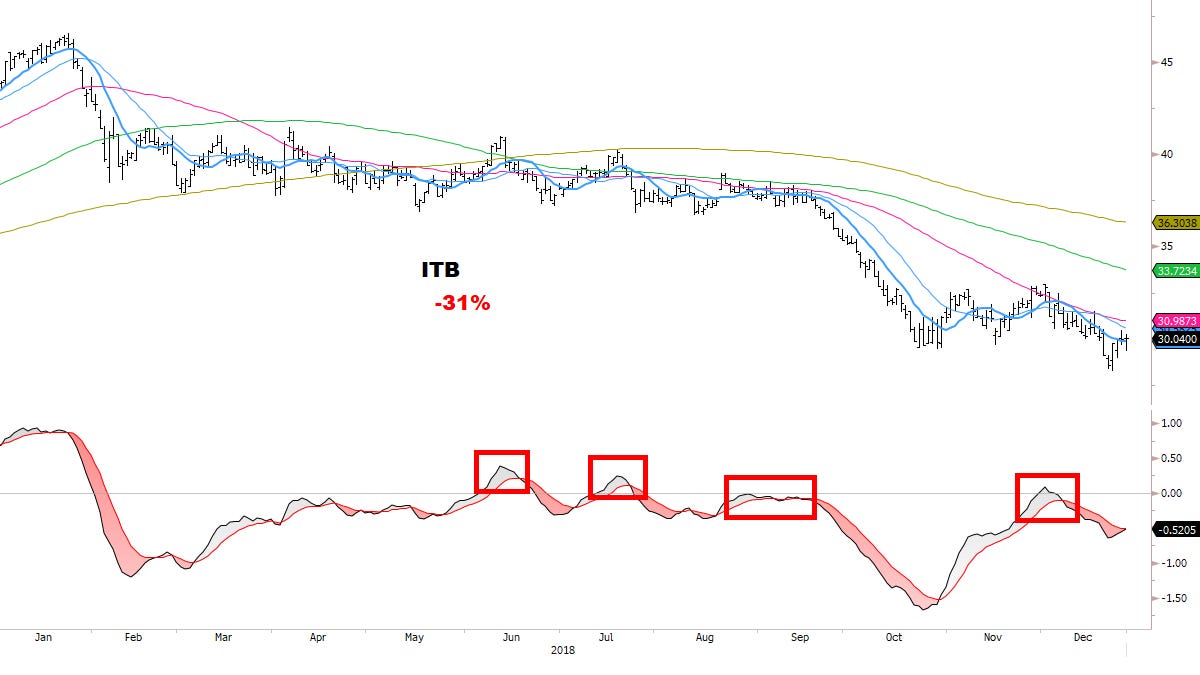

2018

Worst-performing (candidates for Short book):

Best-performing (candidates for Long book):

Only two Sectors were up on the year:

Health Care +3.4%

Utilities +1.3%

VIX 2018 high: 50.

Another year of “WINNER TAKES ALL”.

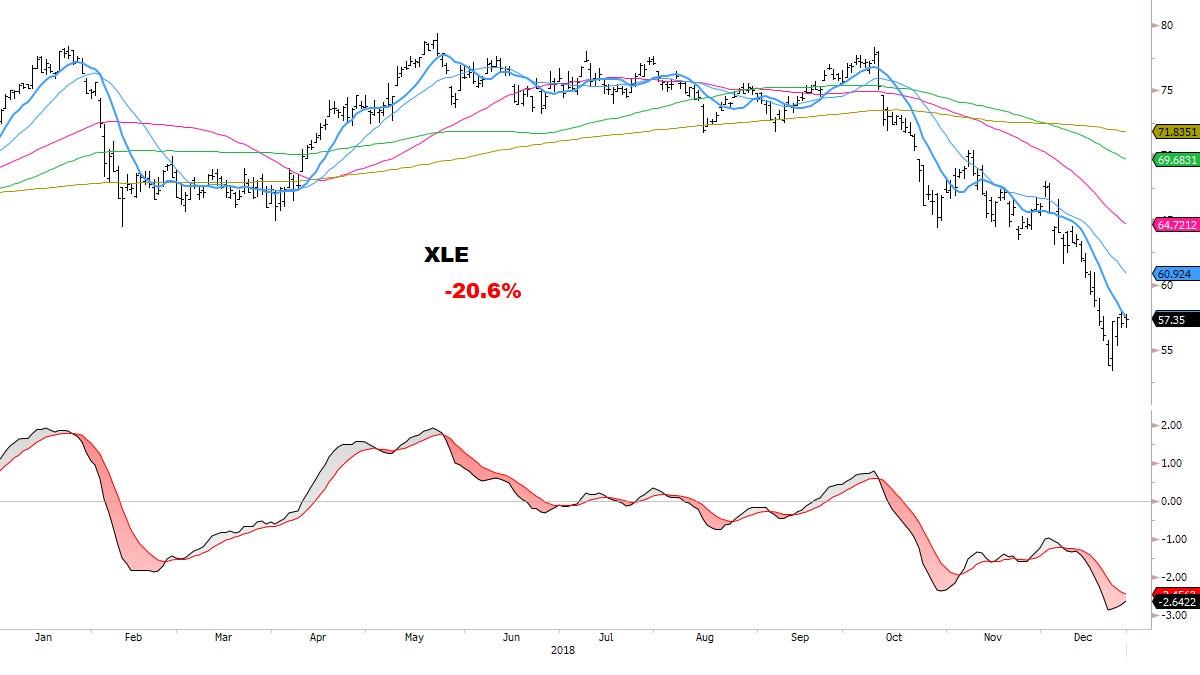

2022

Worst-performing (candidates for Short book):

Best-performing (candidates for Long book):

Only one Sector was up on the year:

XLE +59%.

“WINNER TAKES ALL”.

VIX 2022 high for reference: 39.

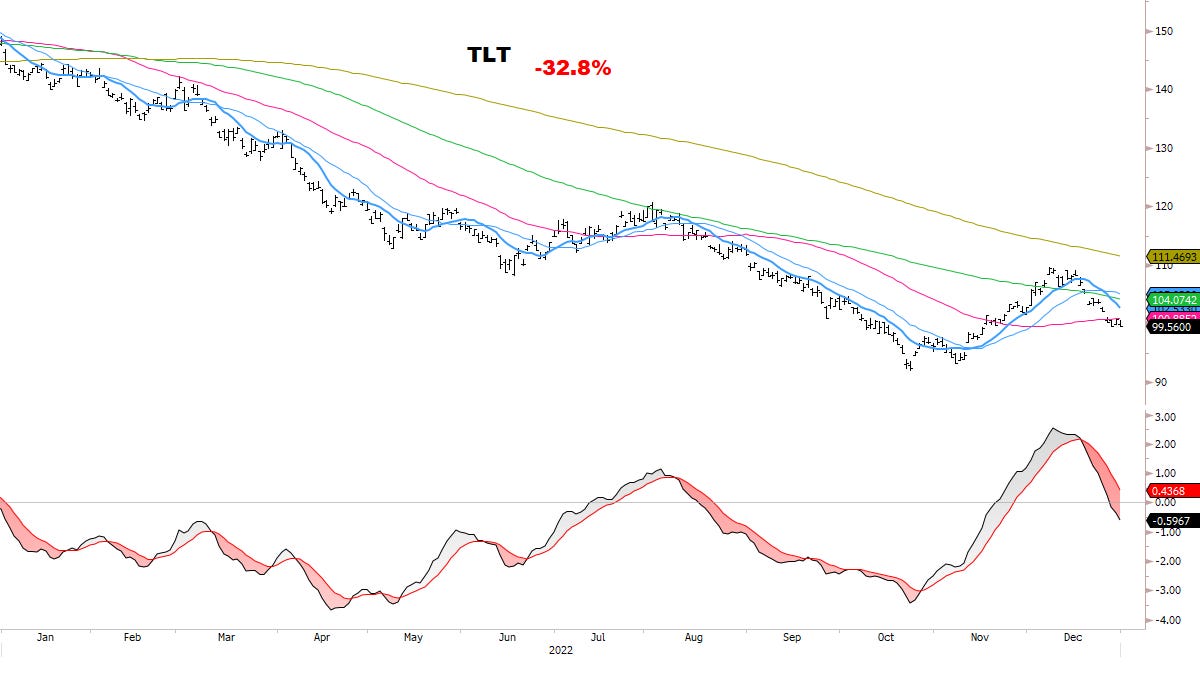

Bonus Charts:

Both charts showed initial weakness in December, failed the bounce attempt, and began major declines — a common pattern.

ESSENTIAL NOTES

To be clear — I don’t think 2025 will be a Bear Market for the S&P.

Still, if you’re a Long-Term Investor, perhaps waiting to add capital incrementally on a 10/15/20% S&P drawdown could be better?

If you’re an active Trader / Portfolio Manager:

First, as we saw in the charts, it didn’t matter if it was a Bear Market.

The key was to focus on the weakest groups, as Shorts/Hedges against Longs.

The S&P tended to mask the Sector damage, and ultimately Volatility was just a wake-up call for the Index.

In the S&P’s biggest decline of those years, the weakest Sectors fell 2-3x more than the Index.

So we want to focus on what’s showing initial weakness.

Right now, there are several leading candidates…

2025

Sectors *potentially* finishing Major Tops / starting larger declines:

Last but not least…

This time of year, I’m watching closely for new downside leaders — especially if they develop failed bounces in the next weeks.

Maybe the Market is giving an early look at next year’s losers from Government policy change and/or economic shifts?

Several areas could be in the early stages of bigger downtrends:

As we saw throughout history, if confirmed, these downtrends could last most of 2025 — so watch the next weeks *carefully*.

I could envision being Short the weakest Sectors next year, while having no Index Shorts at all.

Having an active Short book could be essential.

You don’t have to get every Short right — but the ones that work could be down 2-3x the Index. You could do relatively ok, in a year where Equities chop around violently with big drawdowns. Using Puts tactically could work too.

Of course, there are things to be LONG as well — particularly the areas benefiting from disruption — such as winners from new Government policy, or Defensive assets in a liquidity run…

THINKING ABOUT NARRATIVES

As we said before, Hurricane Years are an upheaval of consensus narratives and crowded positioning.

In this section, let’s think about (1) what kind of disruption we could see, and (2) what isn’t priced in.

And maybe some potential surprises to consider…

The U.S. Government is the country’s largest employer, with 3 Million federal workers (*not including military personnel or postal workers).

For comparison, the largest private employer is Walmart, with 1.5 Million employees in the U.S.

As Marc Andreessen revealed in a recent podcast, after COVID most Government workers never returned to the office. Under some union agreements, they only work 1 day a week from an office. It’s difficult to say how many Government workers currently don’t do any work at all (“mouse jigglers”), but it’s probably a significant number.

Enter Elon Musk — who will be co-Director of the Department of Government Efficiency (DOGE) — and has said all government workers will be required to return full-time to the office.

Keeping in mind that all of Elon’s companies operate this way, and after buying Twitter he fired 80% of the employees within months.

DOGE is not a joke, and it will soon launch at full speed. They’re already ramping up the core teams, and they’re leveraging social media to educate the public on all the excesses of Government spending. Just last week, all of social media got to see the detailed list of “pork” in the debt vote. A revolution is coming…

With many Government workers nearing retirement age anyway (estimates indicate around 25% of federal employees could be retirement-eligible within the next few years), how many Government jobs could realistically be eliminated, either through attrition or reallocation / shifting of resources? Maybe 30-40%? A loss of that many jobs over a 1-2 year period would have a negative impact on U.S. consumer spending.

Further, perhaps the bulk of these changes would be front-loaded, in Year 1-2 of Trump’s presidency (similar to Twitter’s first year under Elon).

Further, Trump is considering privatizing the Postal Service, which loses $10 Billion a year and employs 650,000 workers (separate from the 3 Million federal workers). The USPS would likely see mass layoffs as a private company.

Modernizing Government systems, streamlining payroll and cutting legacy contracts would all have large long-term benefits for the U.S. economy, as resources and capital get reallocated into more efficient areas.

But in the short-term, the front-loaded economic impact would likely be disinflationary.

On immigration, let’s estimate that the deportation of 1MM illegal immigrants per year *in addition* to the base rate, for the next 1-2 years, and the cutting of all associated Government spending and support, would be another potentially disinflationary force. Some transportation and logistics service providers would benefit — but the overall tone would likely be disinflationary.

Further, Health Care is a major component of CPI, and one which “never goes down”. America’s health system is clearly broken. The industry has strangled the golden goose (the American people) through a system of broken incentives for decades, leading to the most inefficient / abused medical system in the world.

Enter Trump — what happens if the government disrupts the way Health Care companies do business? How medical products and services get prescribed, charged, inflated, reimbursed and paid?

The U.S. could see a structural shift in how the government does business with companies. Health Care is one of the core S&P Sectors — and an important part of the economy. How many administrative Health care (non-Medical) jobs are potentially at risk of restructuring?

We don’t know if the next administration will successfully disrupt everything, but the probability they move the ball in that direction is perhaps the highest in a generation.

We should take them at their word that things will change dramatically — disruption is coming. Even a small amount is enough to get Stocks moving sharply. As such, the areas being disrupted are the most vulnerable. That’s what we should be thinking as we scan for new downtrends in 2025. These shifts may have already started.

Short-term, disruption causes pain. Long-term, these changes should help the U.S. to become a more meritocratic system. Companies creating value for the consumer will survive and thrive. And as always, the Stock charts will reveal who they are.

Eventually, spending cuts could create room for targeted, lower taxes — maybe in the back half of Trump’s presidency. But it’s a tight balance, and it should be conducted carefully (or the Bond market could throw another tantrum).

Lastly, we should be aware of other potential disinflationary shocks — such as a European government crisis (low probability at this time), a China currency devaluation in response to escalating trade war (low probability at this time), or a Japan-led GLOBAL repatriation of capital. Of the many disinflationary forces lurking in the sidelines, Japan is a notable concern for me, as discussed previously. We’ll see what happens.

SENTIMENT DISRUPTION

Sentiment is ripe for disruption as well.

At the end of last year, everyone was on recession-watch — which didn’t happen.

Fast-forward to today:

BofA’s latest Fund Survey shows almost no one in the slowdown camp for 2025.

U.S. Equity allocations are at record highs.

Financial Sector allocations are at record highs.

Cash allocations are at record lows.

The most underweighted areas are Cash, Europe, EM, Bonds and Staples.

Funds expect the U.S. to be the best-performing Stock Market next year.

Funds expect the Russell to be the best-performing Index in the world next year.

Funds expect the Dollar to be the best-performing currency in the world next year.

Only 2% of Funds expect Bonds to be the best-performing Asset Class next year (down from 15% just a month ago).

What could disrupt these high expectations?

And remember… disruption brings Volatility:

FINAL THOUGHTS

Hope for the best, but be prepared for tougher Markets next year.

No Short Volatility exposure.

No Margin/Leverage.

Increase Cash buffers as opportunities dry up.

Identifying extreme winners AND losers — and staying with those Trends — could be THE defining opportunity & challenge of 2025.

One day at a time, we’ll be focused on the signals.

And if the winds pick up, we’ll be ready.

Thanks for reading.

Onwards and upwards, -MC

X: x.com/MacroCharts

ABOUT: macrocharts.substack.com/about

FOR NEW READERS — Charts in High-Quality format via Web/App:

As of Feb 8th, this post is now even more relevant than in December. The hurricane is here

Excellent playbook on hurricanes. Much appreciated!