SHORT NOTES: 2/20/2026

Retail Power, No Room For Error, Sentiment Stress, “Push it to the Limit”, and much more.

Good morning and happy Friday — hope everyone had a great week.

In today’s edition:

✅ My collection of BEST recent charts & articles “heard on the street”.

✅ *And adding a few of our own.

Let’s get started…

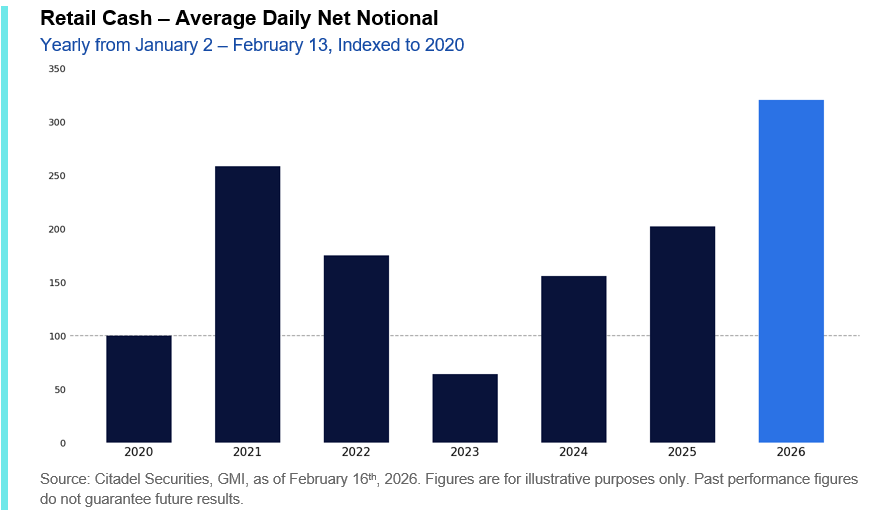

1. Retail Power.

One of the most stunning data compilations I’ve seen…

From Scott Rubner, head of equity & derivatives strategy at Citadel:

“To start the year, retail participation has been unprecedented.

Net notional on our platform has reached levels we have never observed before. The magnitude, persistence, and breadth of buying activity have materially exceeded prior peaks, underscoring retail’s role as a primary source of incremental demand in early 2026.”

“Average daily net notional traded on our platform from Jan 2—Feb 13 is running far above any comparable period in our history – nearly 60% above last year, ~25% above the prior peak in 2021, and double the 2020-2025 average.”

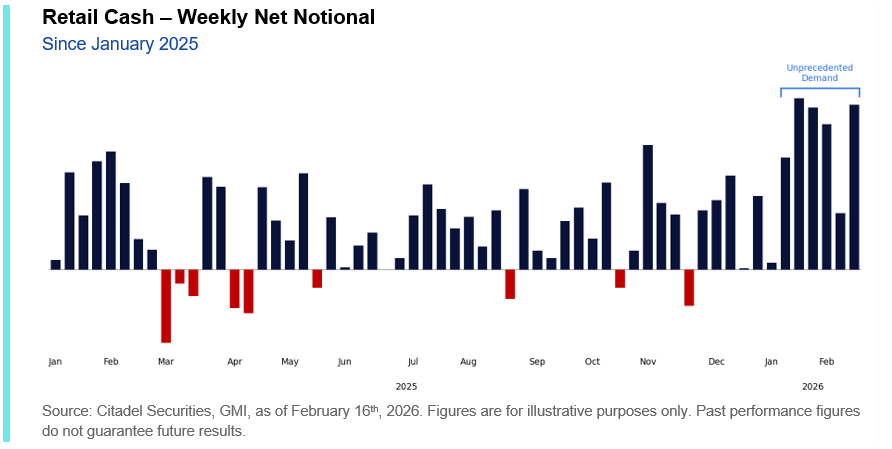

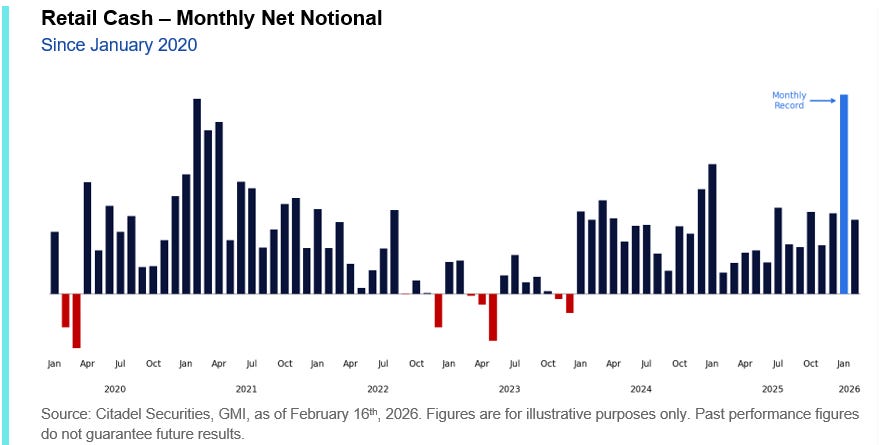

“The activity has been persistent. Zooming out, both weekly and monthly aggregates reinforce the same message: retail has been a sustained and material source of demand across equities to start the year.”

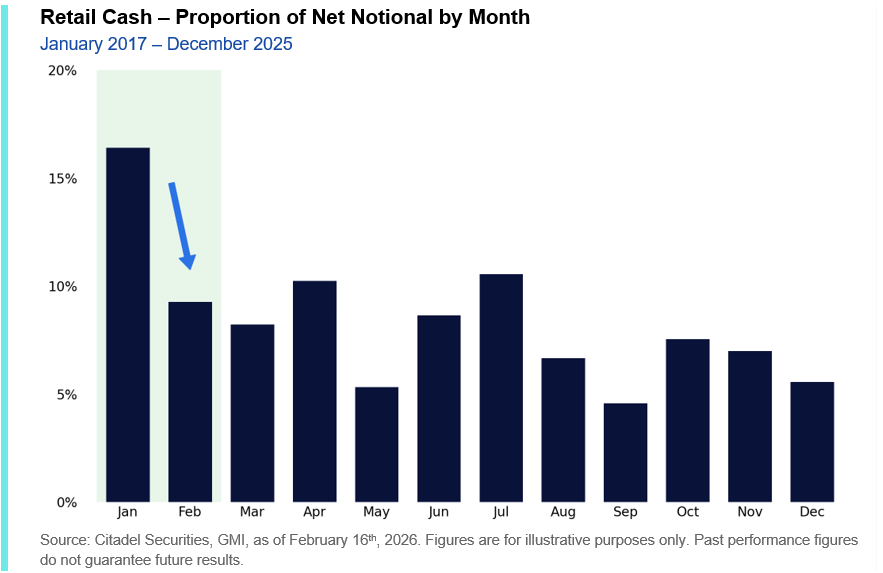

*Above: January was the biggest month of retail flow in Citadel’s history — the last record was at the Meme Bubble peak in Q1 2021.

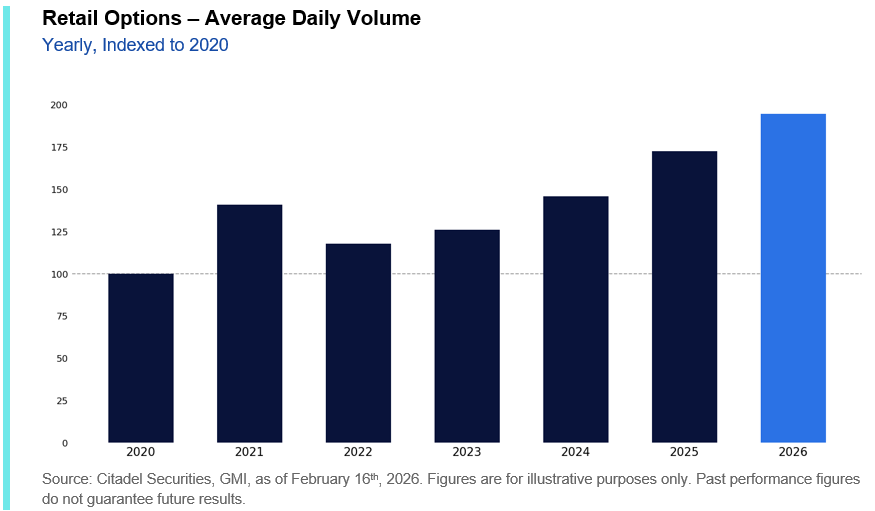

Additionally:

“This strength is not limited to cash equities. Retail options participation in 2026 is already running at historically elevated levels. Average daily options volume year-to-date is more than 15% above last year’s pace and nearly 50% above the 2020-2025 average.”

Are retail investors single-handedly driving the market?

*And if so: what happens when they -slow down- their buying?

Maybe we’ll soon find out:

As Citadel notes…

Retail flows tend to drop after January:

“As we’ve highlighted in prior notes around the January Effect, retail flows are typically front-loaded. January historically represents the largest share of annual net notional, with February stepping down meaningfully in proportion. The seasonal pattern suggests that early-year intensity often moderates as the quarter progresses.”

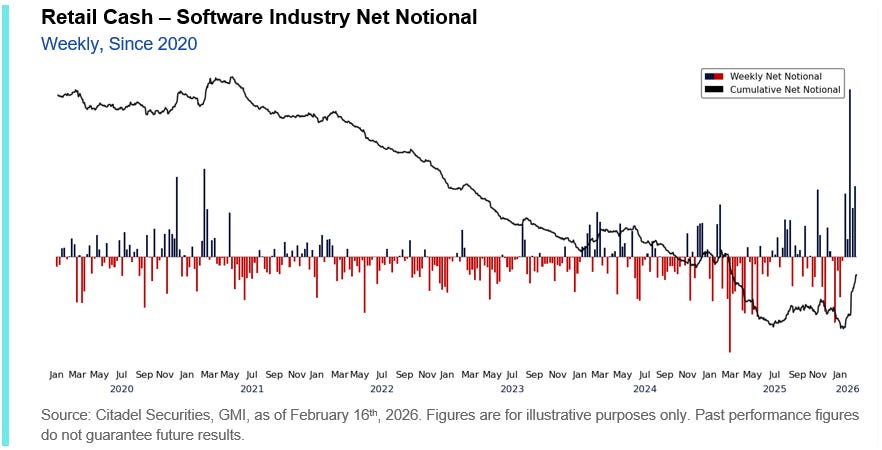

For now, retail flows stayed elevated in February — as investors aggressively bought Software stocks:

“Software is the clearest example – as the group has come under pressure, retail investors have leaned aggressively into the weakness, driving flows decisively into single-stock software names. This buying has reached historically extreme levels.”

The key takeaway:

“February strength has been supported in part by concentrated dip-buying within one of the market’s most volatile segments. If flows were to normalize toward more typical February proportions, the incremental bid behind retail-favored themes – several of which have led year-to-date – could begin to soften. Retail does not need to reverse outright to influence price dynamics. We are monitoring for signs of a moderation in intensity, which could be sufficient to alter momentum in areas that have relied heavily on sustained dip-buying and concentrated participation.”

If the biggest buyer takes a break, what happens?

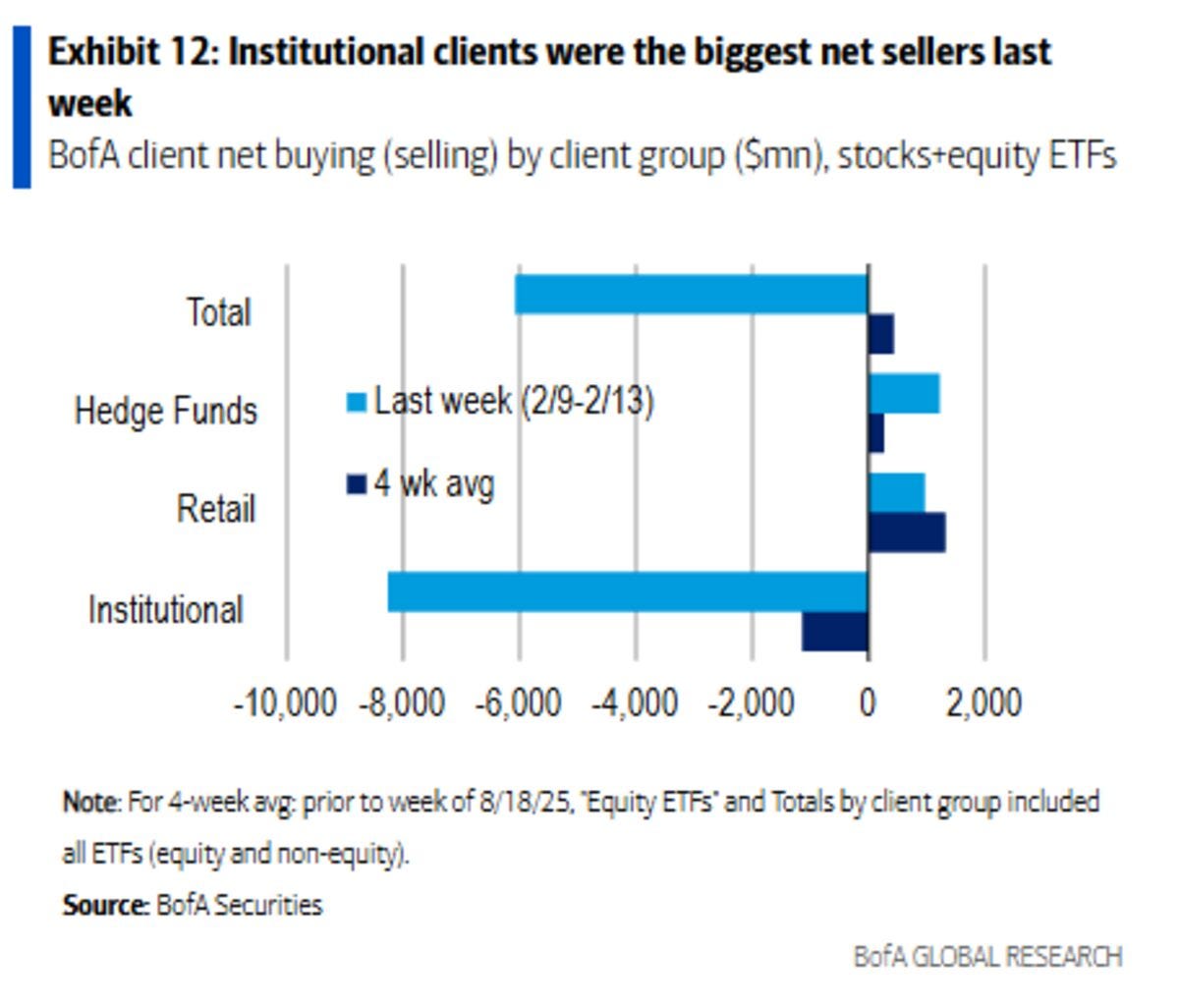

Meanwhile, institutions have been heavy sellers:

“BofA Clients Sold Stocks at Near-Historic Levels”

“Clients dumped US equities last week, with outflows reaching near-historic levels.”

“Outflows were the third highest since records began in 2008.” [$8.3 Billion]

This is a massive tug-of-war brewing:

Who will be right: Retail/HFs or Institutions?

Further, from GS Prime:

“Against a more challenging performance backdrop and tougher technicals, hedge funds have turned more defensive and net sold US equities MTD at the fastest pace since March 25,” the team led by Vincent Lin wrote in a note.

Gross leverage for US long/short funds has fallen by 8.6 points so far in February, the team writes, which is tracking one of the sharpest monthly declines in GS data back to 2016. The reduction almost completely reverses the increase in risk-taking seen in January.

And while this rapid leverage reduction suggests hedge funds are at a late stage of de-risking, overall positioning still remains in an extended phase with US long/short gross exposure in the 96th percentile on a three-year lookback, the Goldman team says. It is therefore “not yet at a level where positioning can become a sustained equity market tailwind,” Lin adds.

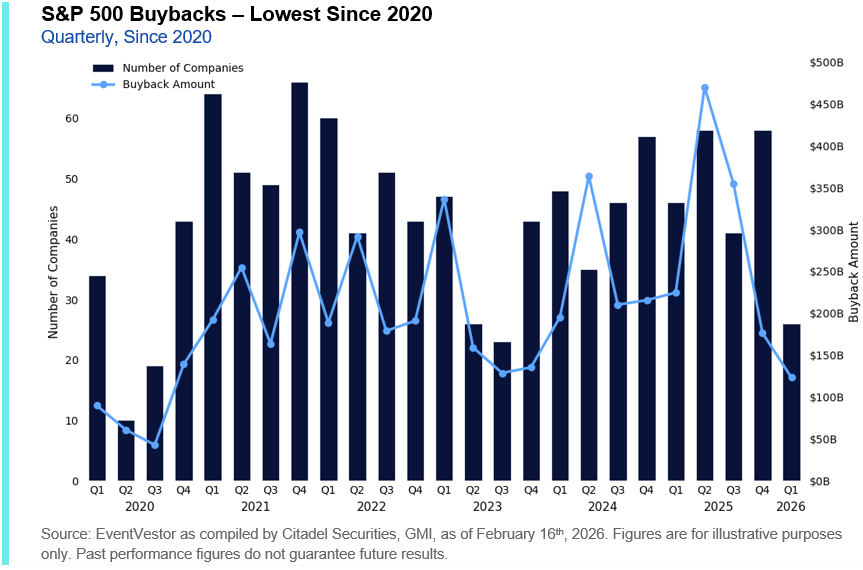

There’s another big buyer which has also faded…

From Citadel:

“The surge in [hyperscaler capex] investment has coincided with moderation in share repurchase activity. Aggregate buyback volumes have softened to their lowest levels since 2020 as incremental cash flow is increasingly directed toward compute, data center expansion, and AI infrastructure.”

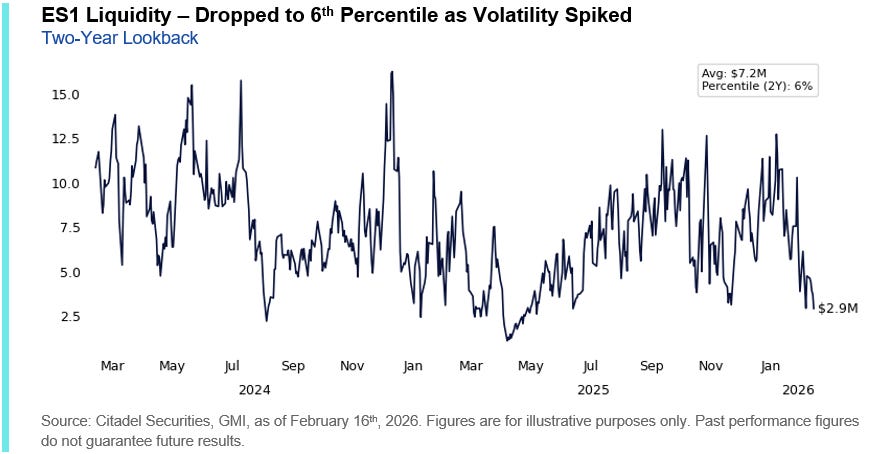

Exacerbating the risks, Citadel notes liquidity has also dropped sharply:

Meanwhile:

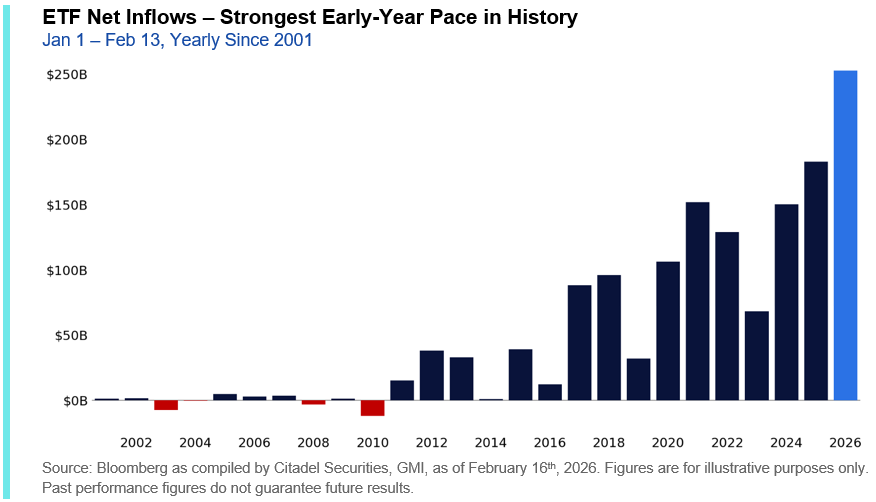

“We are just 31 trading days into the year, yet ETFs have already attracted nearly $253 billion in inflows – roughly 40% higher than at this point last year. For context, the average full-year ETF inflow through 2020 was approximately $244 billion. In just six weeks, ETF flows have already exceeded what once represented a typical entire year.”

What happens next?

We’ll see… but 2026 is already off to a solid start — and promises to get even more interesting.

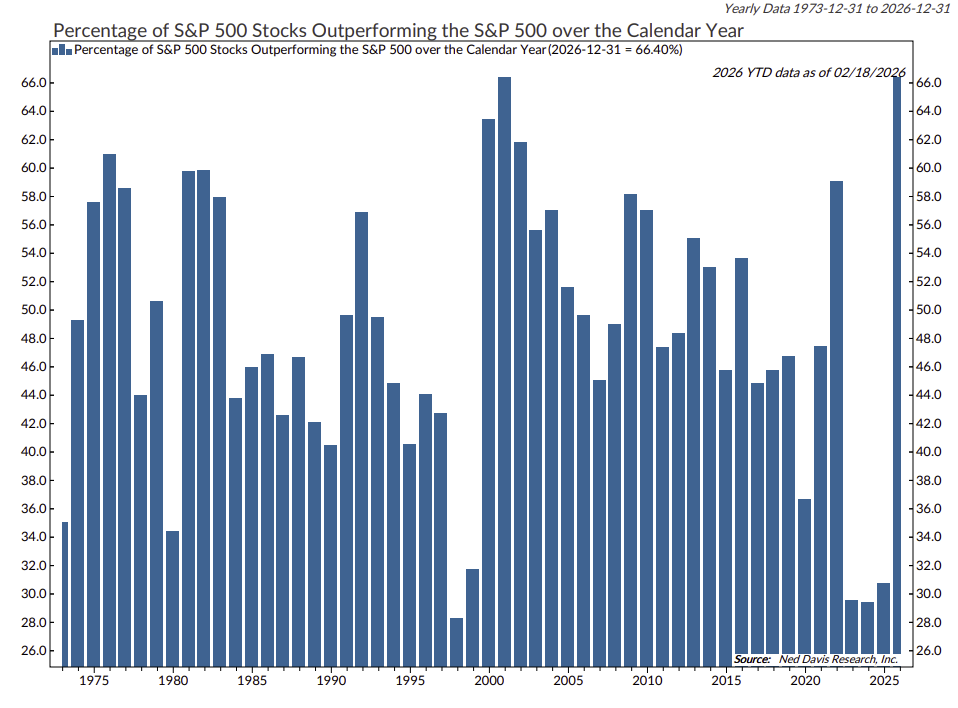

2. Everyone’s Winning (continued).

From NDR:

“At 66.40%, the greatest number of index constituents are outperforming the S&P 500 index itself over the last 50 years.”

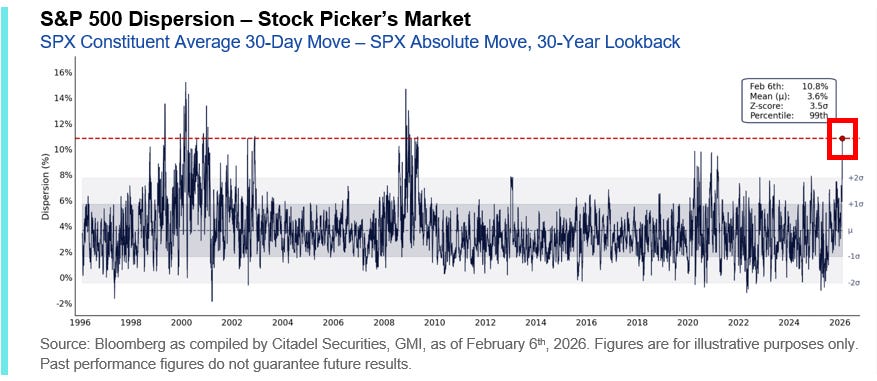

Related, from Citadel:

“Single-stock dispersion is at extreme levels. Over the past 30 days, the S&P 500 is down 1.4%, while the average stock in the index has moved 10% in absolute terms, placing the 8.6% dispersion spread in the 97th percentile over the past three decades. Earlier this month, this spread surged to 10.8% – a 99th percentile event and a 3.5σ outlier over the past thirty years.”

Remember what we wrote the last time this happened:

✅ This chart ties closely with our (1) 2026 framework, (2) diversification strategy, and (3) thematic allocations.

✅ Momentum was KING in 2025, and 2026 could be even stronger.

As Peter Lynch once said:

“Know what you own, and know why you own it.”

3. Fund Manager Sentiment.

Many interesting charts in BofA’s latest survey.

Several themes look stretched — but some are truly extreme:

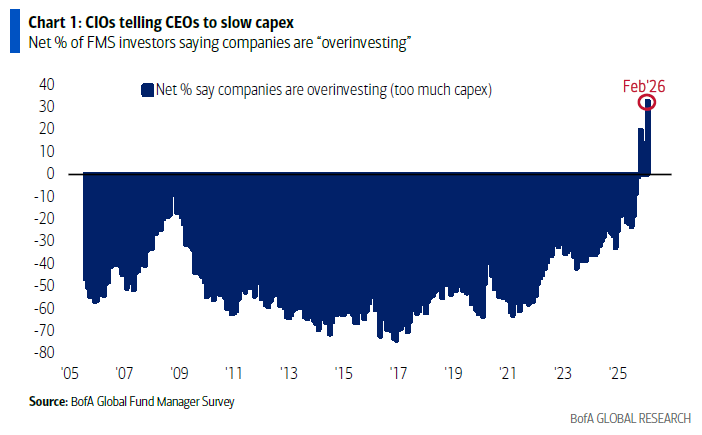

“CIOs are telling CEOs to slow capex”

A record number of investors think companies are overinvesting.

Eventually this will matter — and remember, “Shareholders/CIOs are the boss of CEOs”…

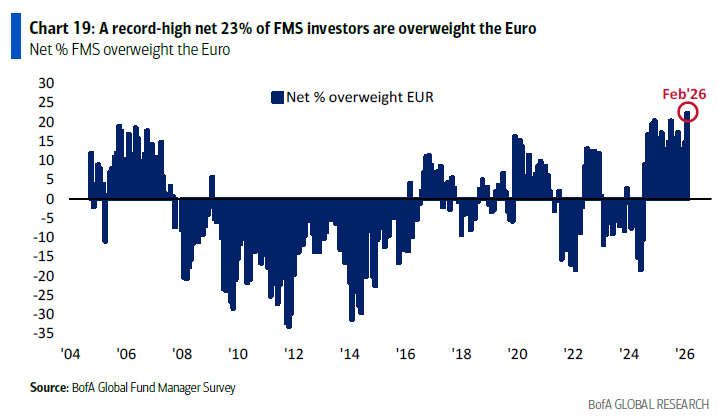

In the FX world, it’s a record-high overweight in Euro positioning:

✅ This is fully aligned with our work on currencies.

Right on schedule…

✅ It looks like the upcoming Barron’s cover will be “The Reign of the Dollar is Coming to an End.”

Here’s a preview:

✅ As a reminder, The Economist ran this cover not even a week ago:

*The article was about: “The age of a treacherous, falling dollar. Those holding American assets will have to get used to it.”

In our upcoming report:

✅ We’ll include a timely discussion on “what a Dollar rally looks like”.

✅ And what we’ll be doing about it.

Strap in…

4. Major Market Shifts.

A fascinating study from Bloomberg:

“S&P Equal Weight outperformance was extremely rare historically”

Prior cases: 1999-2002 Dotcom, 2009 Post GFC, and 2020-2021 Covid.

“Those cases accompanied major shifts in the market.”

“Equal-weight S&P managed to maintain some outperformance 250 days later.”

The big question:

“Whether this is the start of an extended period of sharp moves around AI disruptors, and the disrupted.”

✅ Best guess: why not a bit of both?

✅ Either way: our process will keep us laser-focused on the big opportunities — on disrupted names with potential to recover sharply, or new leading stocks poised to take the helm.

Stay tuned.

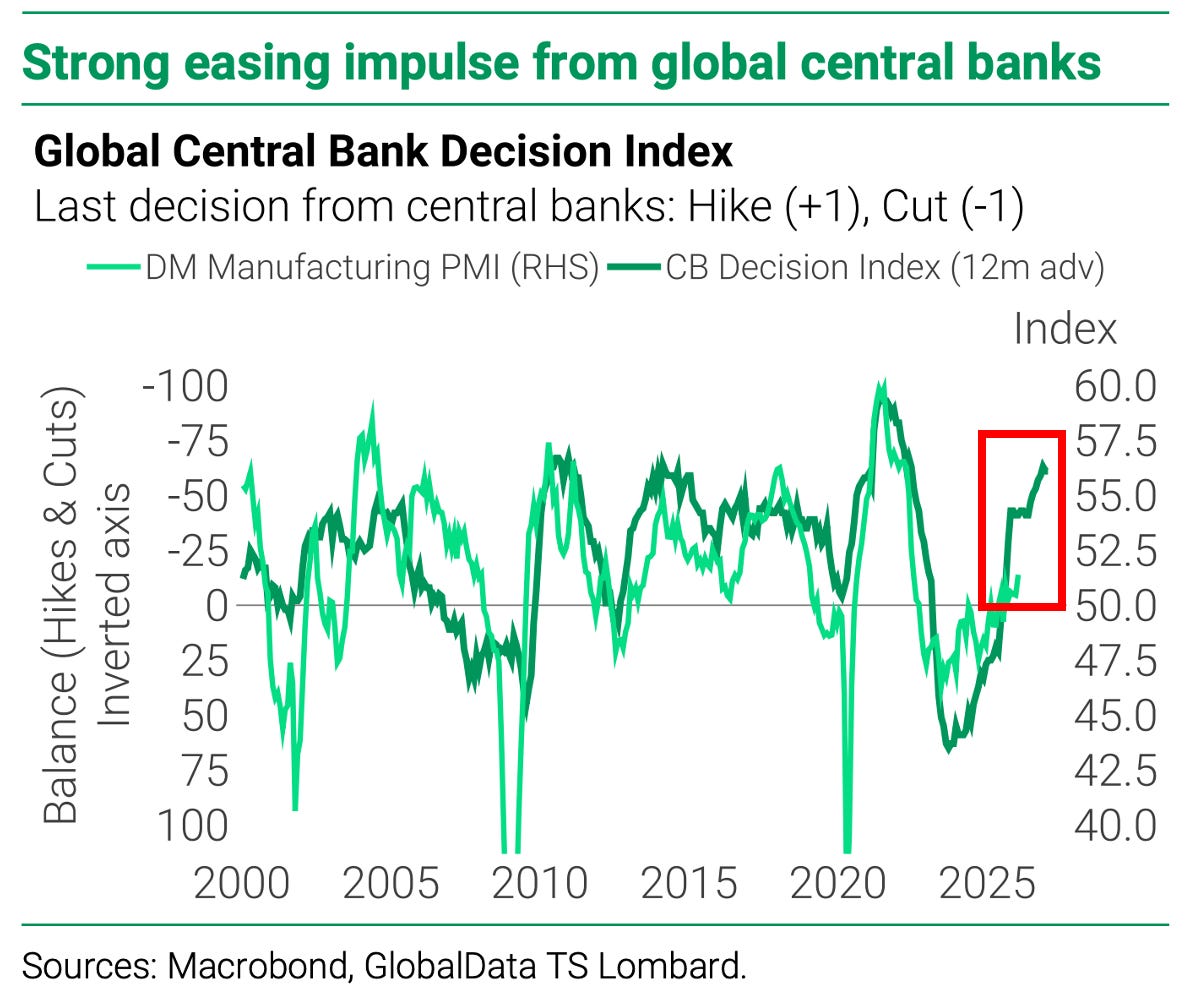

5. Macro Tailwinds.

From Michael Kantrowitz at Piper Sandler:

“The macro data continues to support the broadening narrative which is the other major theme thus far in 2026.”

Michael’s chart shows U.S. PMI and Cyclically-correlated stocks moving higher in lockstep:

Similarly:

TS Lombard shows monetary policy is leading economic activity higher:

Taken together:

✅ These are strong tailwinds, particularly for Cyclical equities — fully aligned with our allocation framework, and strategy.

✅ We’ll stay focused on the trends, looking to the big leaders this year.

Follow the stocks, always…

Opportunities are out there — have to keep looking, and stay disciplined.

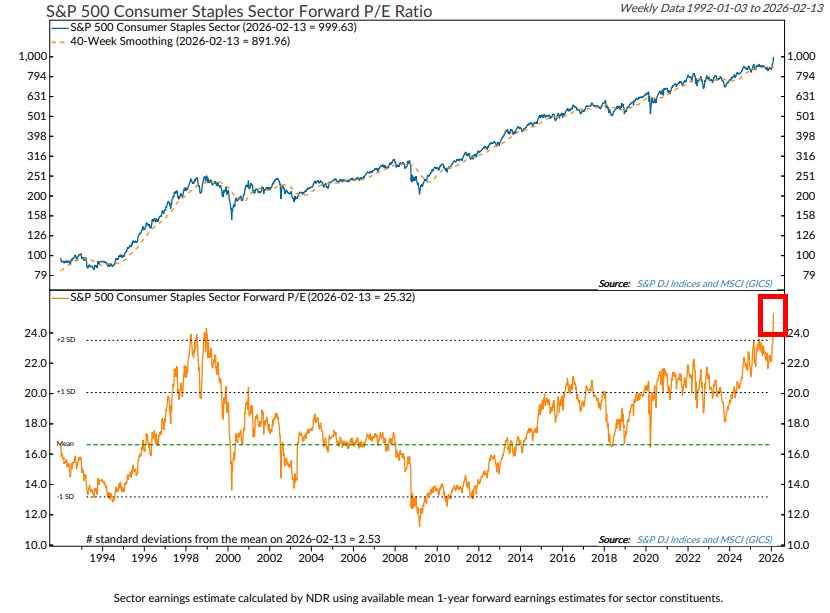

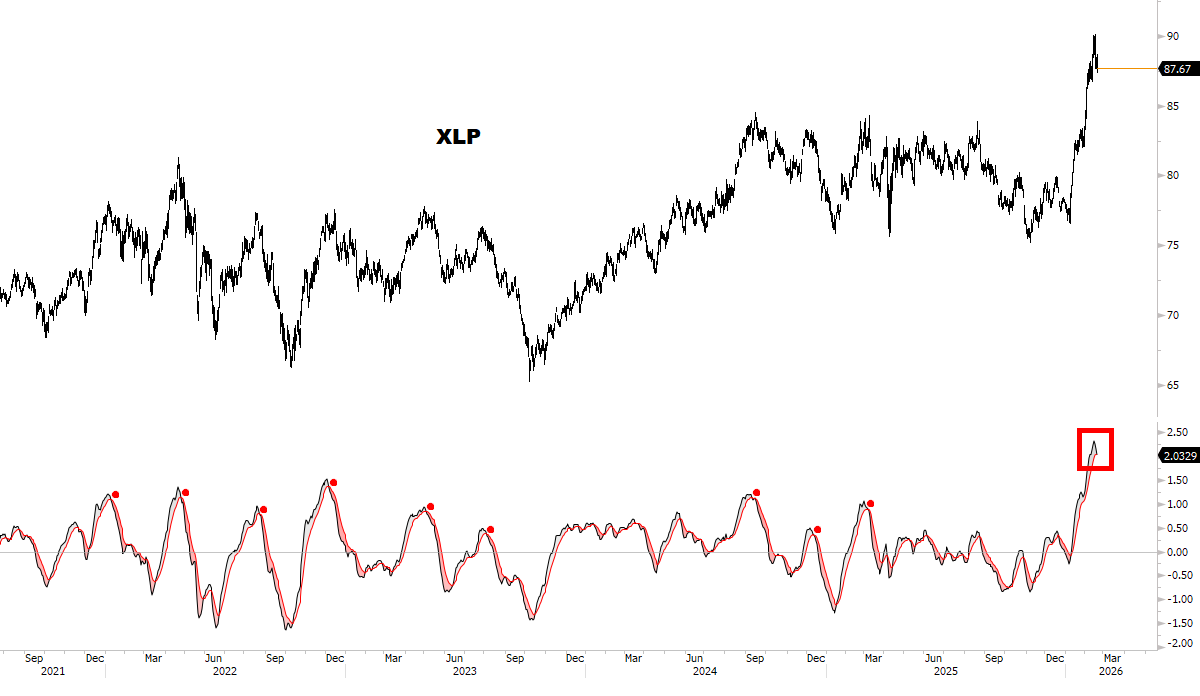

6. No Room For Error.

On the other side of the risk/reward equation:

Consumer Staples are now trading at a record-high forward P/E:

Would Staples correct on their own, or in a broader market decline?

Either way, there’s no room for error in this group.

Tighten up trailing stops…

“Know what you own, and know why you own it.”

7. Market Stress.

A good read on *market stress* from GS:

“Our vol stress index closed the week registering 9 out of 10. Historically, readings of >9 have been buying opportunities, but this time ‘feels different’ as the increase in panic has not come with a decrease in spot prices.

The market is treating this episode as an ‘equity-specific’ and ‘model-specific’ problem, with little sign of panic in credit spreads, bond market volatility, or liquidity.

Without a clear risk-off catalyst to assign the increase in equity volatility to, there’s also no defined walk-back scenario to ‘fix’ the problem.

Single-stock volatility is unlikely to subside any time soon, question is how much of this stress will spill over into the index, and then impact wider macro and cross-asset markets.”

What this means:

✅ Have a plan, and follow it.

✅ Our plan remains the same — and we’ll update the big signals this weekend.

✅ Most of all: watch Volatility.

After this week, some of our scenarios could become ‘base case’…

8. Fear of AI.

Remember when companies mentioned ‘AI’ in conference calls, to boost their stock?

Times have changed…

“AI Risk Is Dominating Conference Calls as Investors Dump Stocks”

Some great quotes & read:

“As usual, markets shoot first and ask questions later”

“The trend is clear: If it’s digital, it’s vulnerable”

“The physical world offers more near-term certainty than the digital space”

Next, my favorite chart this week (in case you missed it), tying our BIG views together — plus some NEW themes emerging, and a contrarian opportunity…

9. “Push it to the Limit.”

Keep reading with a 7-day free trial

Subscribe to Macro Charts to keep reading this post and get 7 days of free access to the full post archives.